Quick Summary:

Every business that works with an inventory needs a reliable way to track it and its costs. The First In First Out (FIFO) method is the most widely used method to do this. This post will walk you through everything you should know about this inventory management method.

You'll walk away knowing:

- What the FIFO method is, how it works, and why it is used in inventory management.

- How does it affect your accounting?

- How to calculate it, along with an example.

- How does it compare with the Last In First Out method and other methods?

- The pros and cons of using it.

Inventory management is a complex process in itself, especially when perishable goods are involved. Add to this the fact that input costs per batch can vary, and the complexity only increases.

The FIFO method (First In, First Out) is an inventory valuation approach where the oldest stock is assumed to be sold first. In South Africa, it is the standard method under IFRS and is widely used by retailers, wholesalers, and manufacturers to track the cost of goods sold.

From an accounting perspective, not having a clearly defined method will result in everything from your stock valuations and tax calculations to, most importantly, profit margins being off. This is precisely why inventory valuation methods like FIFO exist.

What is the FIFO Method?

FIFO, short for First In First Out, plays a dual role in the context of inventories. The first is inventory management, where it is used to control how businesses that deal in perishable goods or those with limited shelf lives or expiry dates clear their inventory, i.e., the oldest items are sold first.

The second is for inventory valuation from an accounting perspective. Let’s look at each in detail.

How FIFO Works in Inventory Management in South Africa?

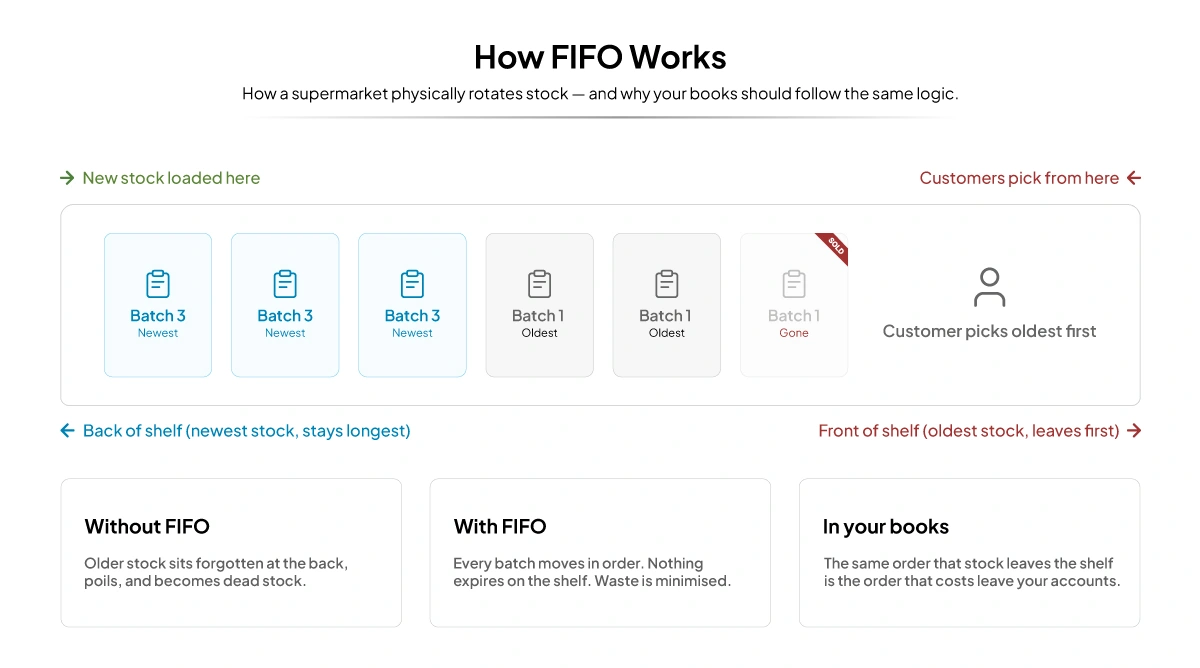

From an operational standpoint, FIFO is a stock movement strategy where the oldest goods in the inventory are sold first.

This strategy is mostly used in supermarkets, pharmacies, food wholesalers, and similar businesses in South Africa that need to physically rotate their stock to

- Prevent dead stock.

- Reduce losses due to spoilt or expired items.

The next time you are at a supermarket, pay close attention to how each product is stacked. You will notice that the items placed in front expire sooner than the ones placed far back.

If you ever wondered why your mother or grandmother always told you to pick something from the back of the shelf, this is why. As a business, following the FIFO method always ensures that your inventory flows in a way that minimizes waste and keeps stock fresh.

For businesses managing multiple sales channels or warehouses, a well-configured order management system can automatically enforce FIFO rules during stock allocation

FIFO in Accounting: How It Affects Your Numbers

From the perspective of accounting, the FIFO method is used to calculate three very important financial values for your business, such as:

Cost of Goods Sold

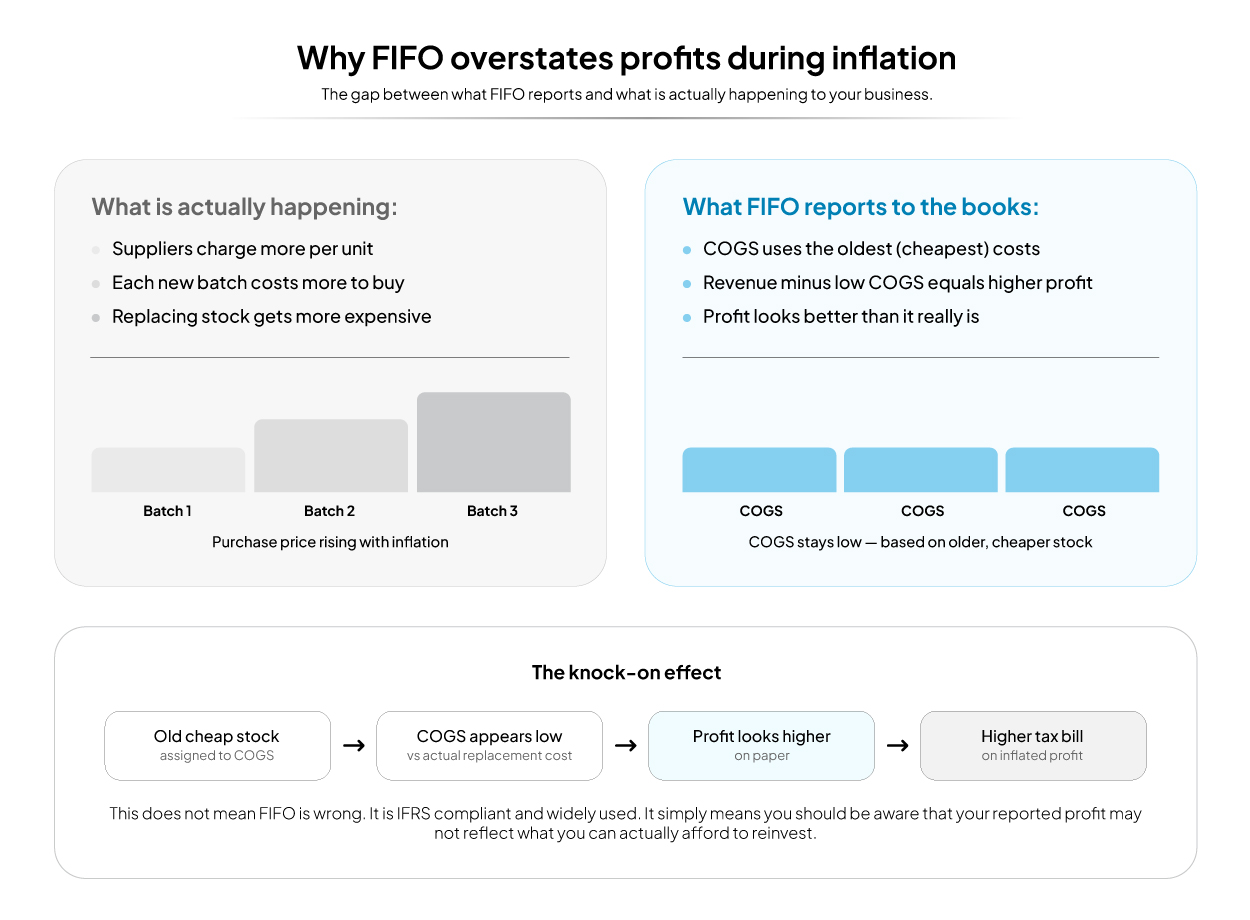

For the uninitiated, Cost of Goods Sold, or COGS for short, is the total cost of the inventory a business has sold during a given period. Under the FIFO method, it is calculated by assigning the cost of the oldest batch to each unit sold first. Once that batch is fully consumed, the cost of the next oldest is used, and so on.

Profit Margins

Now, since FIFO uses older costs to calculate COGS (as opposed to the latest figures that are almost always higher due to inflation), on paper, it makes your business appear even more profitable than it is. On the flip side, this also means higher taxable income.

The Inventory’s Value

Since the oldest inventory is assumed to be sold first, the stock that remains is now valued at the most recent purchase prices. As a result, this means your ending inventory value is closer to the current market value.

Which in turn gives you a more realistic idea of what your stock is actually worth today.

Quick Fact The FIFO method is recognized by the International Financial Reporting Standards (IFRS), which over 140 countries follow, making it the most used inventory valuation method today.

The FIFO Formula

To be clear, FIFO is not a metric in itself, and there is no direct calculation for FIFO. It is, in fact, a method used to calculate the cost of goods sold (COGS). Now, the formula for COGS is always constant, which is:

COGS = Starting Inventory + Purchases − Ending Inventory,

Where:

- Starting inventory: This is the value of all stock your business had on hand at the beginning of the accounting period.

- Purchases: The total cost of all new stock bought during the current period.

- Ending inventory: Is the value of all stock still on hand at the end of the period that has not yet been sold.

Now, the first two parameters are straightforward. The former (starting inventory) is the figure that comes directly from the closing inventory value of the previous period. The latter (purchases) is what you paid for everything you brought in.

What using the FIFO method does is influence the final value of the equation, i.e., the ending inventory.

Since, under the FIFO method of inventory valuation, we assume all the older goods are sold first, you value the ending inventory at the cost of your most recently purchased batches.

FIFO Method of Inventory Valuation

The process to value your inventory under the FIFO method goes like this:

- List all inventory batches in chronological order, noting the quantity and cost per unit for each.

- When a sale occurs, assign the cost from the oldest batch first.

- If the sale quantity exceeds the oldest batch, move to the next oldest batch for the remaining units.

- Continue until the full quantity sold has been costed.

- The remaining unsold units are valued at the cost of the most recent batches.

Example of First in, First Out in Practice

Let’s assume a South African business purchased the following:

- 100 units at R10

- 100 units at R12

- 100 units at R15

This makes the starting inventory value

(100*R10) + (100*R12) + (100*R15) = R1000 + R1200 + R1500 = R3700

Now let’s assume the business has sold 150 units in total. Under the FIFO method of inventory valuation, the assumption will be as follows:

- The first 100 units were sold at R10.

- The next 50 units were sold at R12

Now, let’s calculate the value of the ending inventory. As of now, 150 units remain (50 units at R12 and 100 units at R15. The ending value now becomes:

(50*R12) + (100*R15) = 600 + 1500 = R2100

The formula is:

COGS = Starting Inventory + Purchases − Ending Inventory

Now, if we put the above example into the formula:

We get COGS = 3700 − 2100 = R1600.

Under FIFO, the closing inventory is valued using the cost of your most recently purchased stock. This is what sets FIFO apart from other methods. This assumption that older stock is always sold first directly determines what your ending inventory is worth.

Real-world Examples of FIFO in Action

If you pay careful attention, you will realise that FIFO is used (in both its forms) widely across industries in South Africa.

Grocery Stores and Perishable Goods

Any store that deals with groceries has to contend with limited shelf lives and expiry dates. In this sector, FIFO is the default cause; without it, the losses will eat into their profit margins.

Clothing and Fashion Retail

In the era of fast fashion, clothing stores also adopt the FIFO method to avoid holding onto dead stock or having to give out heavy discounts just to clear it.

Pharmacies and Medical Supplies

Pharmaceuticals carry strict expiry requirements under South African health regulations, so using the FIFO method here is mandatory.

Wholesale and Distribution

For this category of businesses, scale is the biggest hurdle. Using the FIFO method helps them move around the older stock first and track costs consistently. Without it, the losses are on par with the scale of the business.

Advantages of the FIFO Method

Using the FIFO method for both inventory management and inventory evaluation does offer several benefits, such as:

- Realistic and easier stock management: Most businesses naturally sell older stock first, and when the same method applies to both inventory and accounting, it simplifies reconciliation between the two.

- More accurate accounting: Sticking to FIFO in your accounting practices produces a more accurate balance sheet as the closing stock reflects current market prices.

- Reduced waste: FIFO helps reduce waste and the losses that come with it in sections that deal with items with expiry dates and limited shelf lives.

Disadvantages of the FIFO Method

The FIFO method, in some instances, can become a double-edged sword, like so:

- Distorts your profit margins: During inflationary periods, the FIFO method makes your profits look better than they actually are.

- Higher tax liability: The more profits on paper, the higher taxes you pay.

- Does not work well across all industries: For businesses with large, diverse product catalogues where the same items arrive in many different batches at varying prices, FIFO calculations can get quite complex.

FIFO vs LIFO: What’s the Real Difference?

Last in, First out (LIFO) is another method used for inventory evaluation. It’s the direct opposite of the FIFO method and assumes the most recently purchased stock is sold first, leaving older, cheaper inventory on the balance sheet. Here is how the two methods stack up.

| FIFO | LIFO | |

|---|---|---|

| Impact on COGS | Oldest cost assigned to calculate COGS | The latest inventory’s cost is assigned to calculate COGS |

| Reported Profit | Higher during inflation | Lower during inflation |

| Tax liability | Higher | Lower |

Interesting Fact Unlike the FIFO method, the LIFO method only applies to inventory evaluation, and the United States is the only country that allows it. It is not permitted under the International Financial Reporting Standards (IFRS), which South Africa follows.

FIFO vs Other Inventory Valuation Methods

FIFO and LIFO aren’t the only inventory valuation methods available today. Here is how they stack up against FIFO.

FIFO vs Weighted Average Cost

The weighted average cost method averages the purchase cost of each item instead of in batches. As a result, smooths out price fluctuations from the calculations but is less precise than FIFO.

That said, it is simpler and works better for businesses that hold large volumes of identical products, which makes tracking costs per batch impractical.

FIFO vs Specific Identification

Specific identification is a method that tracks the actual cost of each item and assigns that exact cost when the item is sold. It is the most accurate of all the evaluation methods, but it isn’t practical for all businesses.

Quick Fact Specific Identification works best for those who sell high-value items at low volumes.

How ERP Software Makes FIFO Calculation Easy

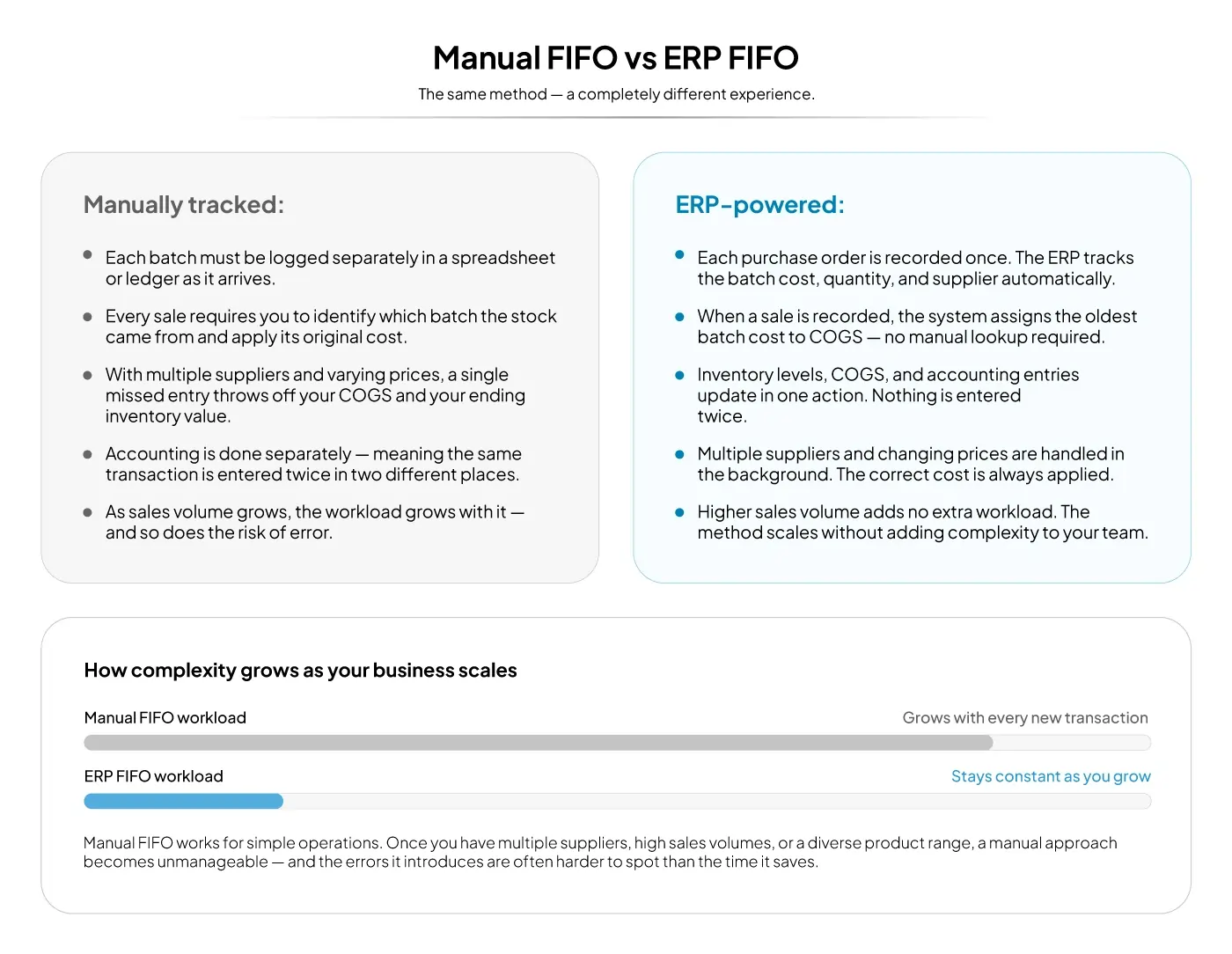

The example given previously in this blog may give a false impression that calculating COGS using the FIFO method is easy.

In reality, once you take into account real-world factors like multiple suppliers and constantly changing prices, to name a few, with high sales volumes, the math becomes impossible to manage manually.

ERP systems simplify this process because they:

- Can track prices across batches from multiple vendors simultaneously.

- Apply the same validation method without any errors across transactions.

All of this is possible because they link your inventory software with sales and accounting on a cohesive platform.

FIFO is Simple, if Your System is Right

At its core, the FIFO method is straightforward, but its calculation gets complex in real-world business scenarios. This is where VasyERP, a cloud-based ERP system, makes a real difference.

It links your inventory, purchasing, and accounting into one seamless system, which then makes it easy to compute FIFO calculations with ease.

With detailed valuation reports and features like real-time stock tracking, you gain insights into fast- and slow-moving items, and your team always knows exactly where your inventory stands and what it is worth.

If you want to see how VasyERP handles inventory valuation for your retail, wholesale, or manufacturing business in South Africa, a 30-minute live demo is all it takes.

FIFO is common in grocery retail, pharmacies, food wholesale, clothing and fashion retail, and distribution businesses. It is widely used in any industry where perishable goods or time-sensitive stock are involved.

FIFO uses older, lower costs to calculate Cost of Goods Sold, which results in higher reported profit and therefore higher taxable income.

Without a clear method, your stock valuation, cost of goods sold, profit margins and tax calculations can be inaccurate, leading to poor decisions and potential compliance issues.

Dead stock is inventory that cannot be sold, usually because it has expired or become obsolete. FIFO helps reduce dead stock by ensuring older inventory is sold first, preventing items from sitting unused until they expire.

During inflation, older inventory purchased at lower prices is used first for cost calculations. This results in lower cost of goods sold and higher reported profit, which can increase tax liability and may not reflect current cost realities.

Last Updated on June 28, 2026